Typical Answers To Home Mortgage Questions

Content create by-Kragelund MahlerAre you curious about what a mortgage is? A mortgage is a long-term loan that is secured by your property. If you are in default of the loan, your house will be repossessed from you. Taking out https://www.businessinsider.com/personal-finance/best-banks-and-credit-unions-florida is huge, so the tips below are important to help you through the process correctly.

Remember that the interest rate isn't the most important part of a mortgage. You also have to think about closing costs, points and other incidentals. There are different kinds of loan as well. That is why you have to find out as much as you can about what you're eligible for.

To make your application for a mortgage fast and easy, make electronic copies of your last two pay checks, two recent bank statements, W2s, and tax information. Lenders will ask for all of this information to go with the application and having them on hand in electronic format makes it easy to supply this information.

You should always ask for the full disclosure of the mortgage policies, in writing. https://www.fitchratings.com/research/banks/fitch-upgrades-hvb-to-bbb-on-unicredit-upgrade-outlook-negative-17-12-2021 ought to include closing costs and other fees you need to pay. Most lenders will be honest about the costs, but there are some that will try and get one over on you.

What do you do if the appraisal does not reflect the sales price? There are limited options; however, don't give up hope. You can dispute the appraisal and ask for a second opinion; however, you will need to pay for the appraisal out of your pocket at the time of the appraisal.

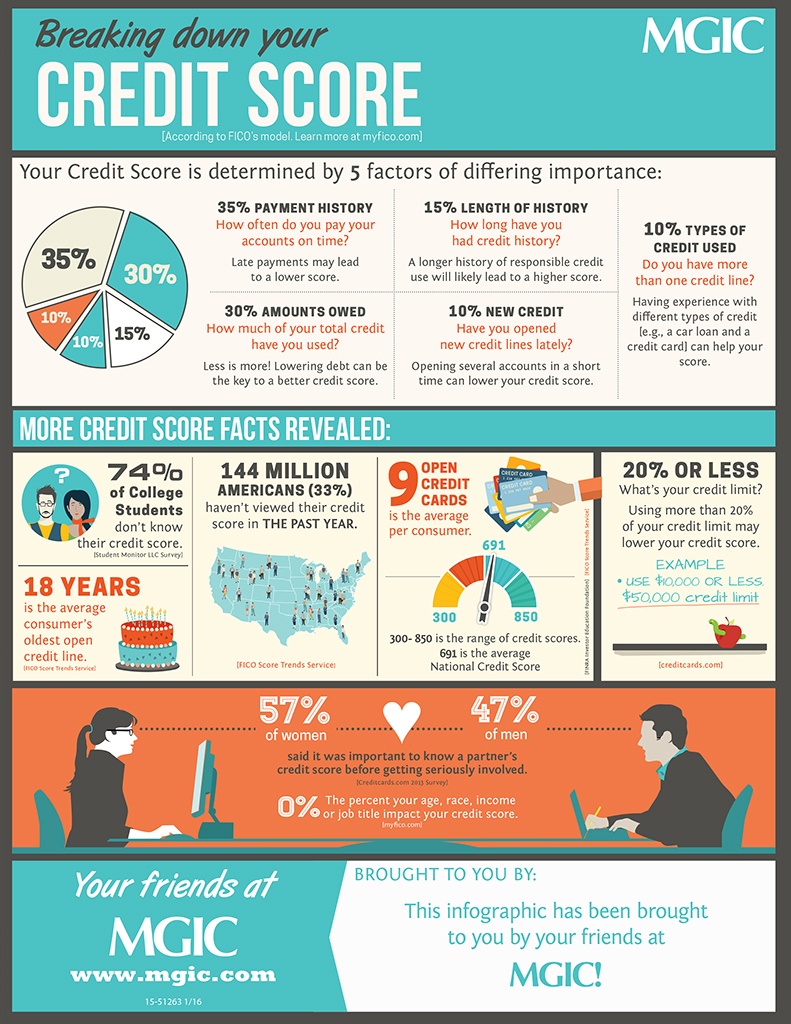

Obtain a credit report. It is important to understand your credit rating before you begin any financial undertaking. Order reports from all 3 of the major credit reporting agencies. Compare them and look for any erroneous information that may appear. Once you have a good understanding of your ratings, you will know what to expect from lenders .

Consider a mortgage broker for financing. They may not be as simple as your local bank, but they usually have a larger range of available loans. Mortgage brokers often work with numerous lenders. This allows them to personalize your loan to you more readily than a bank or other finance provider.

Do not pay off all of your old bills until you have talked to a mortgage consultant. If your bills will not have a negative impact on your ability to get a loan, you can worry about paying them later. You don't want to spend lots of money to pay them since this can affect the amount of available income you have.

If you have a little bit more money to put down on a home, consider getting a conventional mortgage as opposed to an FHA mortgage. FHA mortgages have lower down payments, but excessive fees that are added to the cost of the mortgage. Save up at least 5 percent in order to be eligible for an FHA loan.

Try lowering your balance on different accounts instead of having a few accounts with an outstanding balance. If possible, keep all your balances under half of the limit on your credit. If you're able to, balances that are lower than 30 percent of the credit you have available work the best.

Cut down on the credit cards you use before you get a house. You look financially irresponsible if you have many credit cards. Having a low amount of credit cards can help you get a better interest rate.

If you have a little bit more money to put down on a home, consider getting a conventional mortgage as opposed to an FHA mortgage. FHA mortgages have lower down payments, but excessive fees that are added to the cost of the mortgage. Save up at least 5 percent in order to be eligible for an FHA loan.

Think about your job security before you think about buying a home. If you sign a mortgage contract you are held to those terms, regardless of the changes that may occur when it comes to your job. For example, if you are laid off, you mortgage will not decrease accordingly, so be sure that you are secure where you are first.

Do not even bother with looking at houses before you have applied for a home mortgage. When you have pre-approval, you know how much money you have to work with. Additionally, pre-approval means you do not have to rush. You can take your time looking at homes knowing that you have money in your pocket.

Create a strong relationship between you and your financial institution. Take a small loan out and pay it off before you get a home mortgage. This puts you in good standing with them ahead of time.

The best way to be sure that you take a mortgage which will continue to be easy to pay off in the future is to take less than the maximum amount you are offered. If you have some extra money at the end of the month, you can put it away into an emergency fund instead of your mortgage.

Make your goal to be mortgage free as soon as possible. If you have a line of credit on your home, you can achieve this goal faster by having all of your income deposited to your line of credit instead of your bank account. Withdraw only what you need for other bills and your mortgage will begin to shrink.

If you're not a good negotiator, hire a mortgage broker. The lender will pay their commission, which means you don't have to pay for their help, which saves you time and money. They'll be able to locate a great rate with great terms for you without any time spent on your part.

With the advice that has been given to you, you are now equipped to enter the mortgage market and begin deciding which route you want to take. It's important that you understand all of your options, and you want to feel in control and not thrown into a mortgage by a lender that doesn't fit your needs. Instead, go forth and get the right mortgage!